E-Commerce Disruption in the Jewelry Market in Europe: From Brick-and-Mortar to Click-and-Order

Europe’s value relies on "premiumization." Consumers are buying fewer items, but they are choosing higher quality and ethical standing. The US$ 89.4 Billion figure sets a massive baseline.

Traditionally, the velvet-rope experience of boutiques in Milan, Paris, and London defined the allure of the Europe jewelry market. However, a seismic shift is currently underway. We are witnessing a historic transition where centuries-old craftsmanship meets the high-speed demands of the digital age. While the tactile "touch-and-feel" nature of luxury goods once protected physical stores from digital disruption, 2024 has proven that even the most high-ticket items are finding a home in the digital cart.

This transformation is not merely about launching websites; rather, it is about a fundamental change in consumer psychology. European shoppers are increasingly comfortable purchasing diamonds, gold, and platinum via smartphones. Certified trust seals and augmented reality technologies drive this confidence. In this analysis, we explore the data behind this disruption, leveraging recent findings to understand how the industry is moving from brick-and-mortar exclusivity to click-and-order accessibility.

How Big is the Current Europe Jewelry Market?

As of 2024, the market size has reached a significant valuation of US$ 89.4 Billion.

This figure represents more than just sales volume; it highlights the resilience of the luxury and semi-luxury sectors in Europe. According to recent data from the IMARC Group, the market has maintained this robust valuation despite global economic headwinds. The stability of the European market is rooted in a cultural appreciation for personal adornment. Additionally, a strong gifting tradition persists regardless of inflation.

Furthermore, this valuation reflects a mature market. Unlike emerging economies where growth comes from new consumers entering the market, Europe’s value relies on "premiumization." Consumers are buying fewer items, but they are choosing higher quality and ethical standing. The US$ 89.4 Billion figure sets a massive baseline. It indicates that even a fractional shift toward e-commerce represents billions of dollars in digital revenue. Consequently, experts analyze that this high valuation attracts global investors who view European heritage brands as safe harbors during volatile economic times.

What Is the Projected Growth Rate Through 2033?

Experts forecast the market will reach US$ 107.9 Billion by 2033, exhibiting a CAGR of 2.1% during the forecast period (2025-2033).

While a 2.1% CAGR might appear modest compared to the tech sector, it represents steady, sustainable expansion in the context of a centuries-old heritage industry. This forecast suggests that the market is not relying on a bubble of hype. Instead, it is building on solid foundations of demand. The "click-and-order" phenomenon fuels this growth, as brands expand their reach beyond major capital cities to service customers in remote areas via logistics networks.

Financial analysts suggest that this growth curve will likely be non-linear. We anticipate a faster acceleration in the latter half of the decade. This will happen as "digital native" Gen Z consumers reach their peak earning years. These consumers do not view online luxury purchases as risky; they view them as standard. Consequently, brands that fail to align with this 2.1% growth trajectory by ignoring digital channels risk losing market share to agile, Direct-to-Consumer (DTC) competitors.

Which Jewelry Segments Are Dominating Sales?

Rings currently hold the largest market share at approximately 36.3%, followed closely by necklaces and earrings.

Why do rings dominate the landscape so heavily? The answer lies in the emotional significance and cultural mandates surrounding them. Engagement rings and wedding bands remain non-negotiable purchases for millions of Europeans annually. The 36.3% market share identified in the segmentation data underscores that milestone events remain the primary driver of jewelry revenue.

However, the way consumers buy these rings is changing. Previously, a couple would visit a local jeweler. Today, they might browse thousands of designs on Instagram or customize a ring using a 3D configuration tool. Finally, they might only visit a store for the final sizing - or order it directly with a "perfect fit" guarantee. Following rings, the necklace and earring segments are seeing faster adoption in the e-commerce space. They pose fewer sizing challenges than rings, making them ideal entry points for online luxury shoppers.

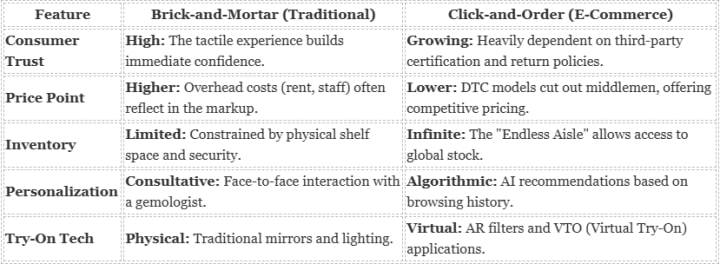

Brick-and-Mortar vs. Click-and-Order: How Do They Compare?

Physical stores still command roughly 84.3% of distribution due to the "trust factor," while online channels excel in price transparency and inventory depth.

Despite the digital buzz, the jewelry market remains one of the last bastions of physical retail. The transition is happening, but the physical store is not dying - it is evolving. To help you evaluate where the value lies for both businesses and consumers, we have compiled a comparison of the two dominant business models.

This table illustrates that while e-commerce wins on price and choice, physical stores win on immediate trust. Therefore, the future winners in the Europe jewelry market will be those who bridge this gap - perhaps using showrooms for trying and apps for buying.

Why Is the Industry Shifting Toward Digital Channels?

The integration of Virtual Try-On (AR) technology and the rising popularity of Lab-Grown Diamonds among younger demographics drive this shift.

Technology has finally caught up with the aesthetic demands of jewelry. In the past, buying a diamond online was a gamble. Today, high-definition 360-degree videos and Augmented Reality (AR) allow buyers to see how a necklace drapes or how a ring sparkles under different lighting conditions. This reduces the return rate, which has historically been the bane of e-commerce profitability.

Simultaneously, the product itself is changing. Lab-grown diamonds are disrupting the supply chain. These stones, chemically identical to mined diamonds but significantly cheaper, appeal to the ethical and budget-conscious sensibilities of European Millennials and Gen Z. Because these consumers are digital-first, they are more likely to discover and purchase these new-age products via social media ads rather than traditional jeweler windows. This synergy between new tech and new products acts as the engine behind the "click-and-order" revolution.

Which European Countries Are Leading the Market?

Italy remains the luxury capital of the trade, followed closely by France, Germany, and the United Kingdom.

Geography plays a pivotal role in market dynamics. Italy is not just a market; it is a brand in itself. The "Made in Italy" tag commands a premium that drives export numbers significantly. However, when we look at e-commerce adoption, the United Kingdom and Germany often lead the pack due to high internet penetration rates and a comfort with distance selling.

France continues to house the headquarters of the world's most powerful luxury conglomerates (like LVMH and Kering). These giants are currently investing heavily in their digital infrastructure, effectively dragging the entire European market forward. As these nations compete, the consumer benefits from better logistics, faster shipping, and more competitive pricing across the continent.

Conclusion: The Omnichannel Future

The data from IMARC Group paints a clear picture: the Europe jewelry market is growing, stable, and digitizing. With a projected value of US$ 107.9 Billion by 2033, the opportunity for growth is immense. However, the "Brick-and-Mortar vs. Click-and-Order" narrative is ultimately a false dichotomy.

The most successful brands are not choosing one over the other; they are merging them. They use physical stores to build brand equity and digital channels to harvest sales. As virtual try-on technology improves and delivery networks become faster, the friction of buying jewelry online will continue to dissolve. For investors and retailers alike, the message is clear: adapt to the digital disruption, or risk becoming a relic of the past.

About the Creator

Joey Moore

I'm Joey Moore, a seasoned Research Analyst with 5+ years of experience in market research. Expert in data analysis, strategic planning, and industry insights. Proven track record in delivering actionable reports.

Keep reading

More stories from Joey Moore and writers in Journal and other communities.

The $1.7 Billion Question: Where is the Europe Real Estate Market Headed?

Europe stands at a pivotal crossroads where historic architecture meets urgent modern demands. As investors and stakeholders navigate the Europe real estate market, they face a landscape defined by rapid regulatory changes and shifting demographic needs. The fundamental question is no longer just about location; it is about value, sustainability, and future-proofing assets against a volatile economic backdrop.

By Joey Mooreabout 15 hours ago in Journal

One Unchecked Box

"Republished" because it was the only way to add the embed for the newly recorded audio version of this story due to the Top Story badge. Plus it serves as a nice, informal announcement of the podcast's revival for another season (go subscribe!):

By Stephen A. Roddewig6 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.