Vacuum Insulation Panel Market Size and Forecast 2026–2034

How High-Performance Thermal Insulation Is Reshaping Construction, Cold Chain Logistics, and Energy-Efficient Appliances Worldwide

Vacuum Insulation Panel Market Overview

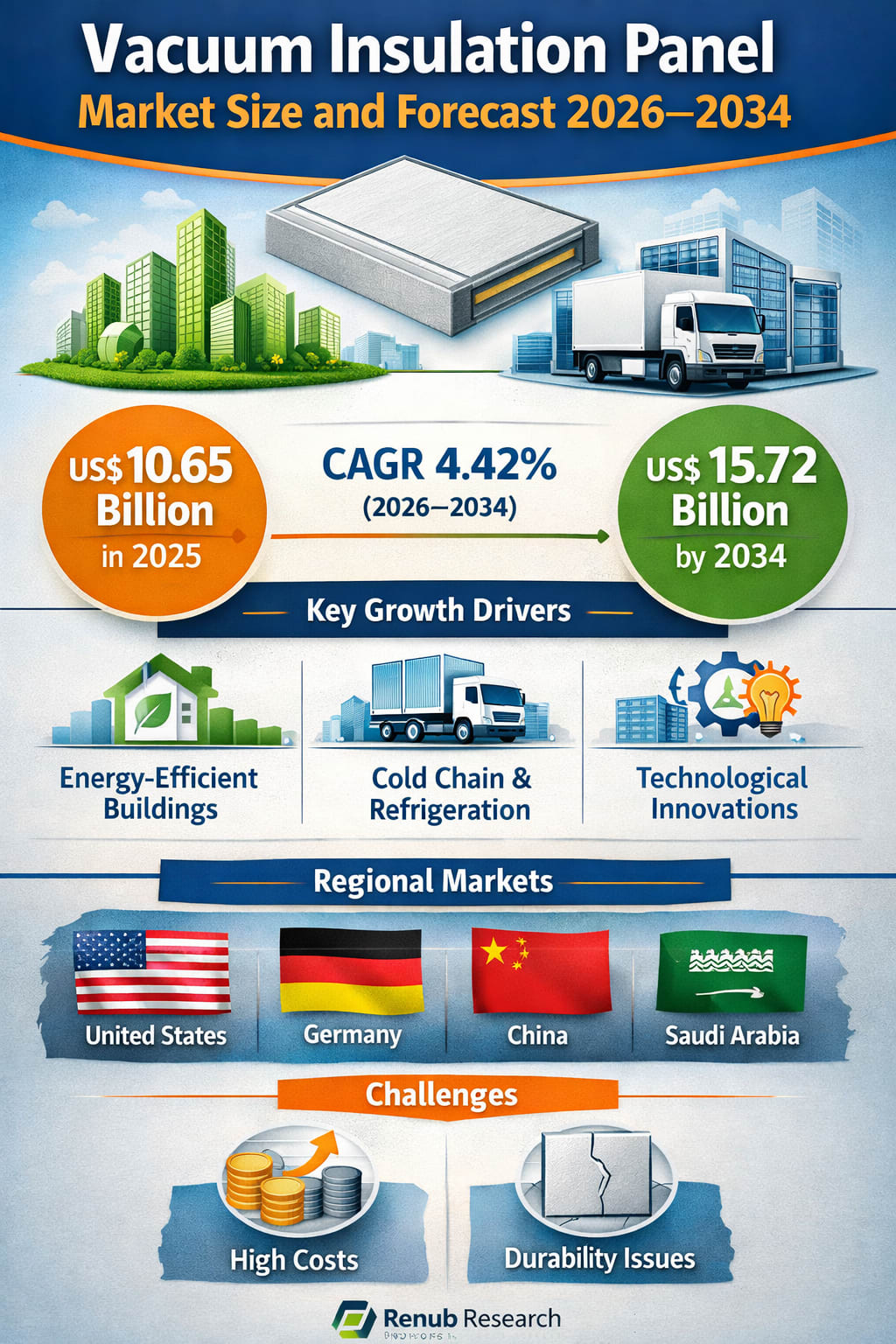

The global vacuum insulation panel (VIP) market is entering a phase of steady and strategic expansion, driven by the urgent need for high-performance thermal insulation across construction, refrigeration, appliances, and cold chain logistics. According to Renub Research, the vacuum insulation panel market is expected to reach US$ 15.72 billion by 2034, up from US$ 10.65 billion in 2025, growing at a CAGR of 4.42% from 2026 to 2034. This growth reflects a broader shift toward energy-efficient materials, space-saving designs, and sustainable infrastructure development worldwide.

Vacuum insulation panels are advanced insulation materials made by enclosing a core material within an airtight barrier and removing the air to create a vacuum. This structure results in extremely low thermal conductivity—significantly lower than traditional insulation materials such as polyurethane foam, polystyrene, or fiberglass. In practical terms, this means VIPs can deliver the same or better insulation performance using much thinner panels, making them ideal for applications where space is limited but performance demands are high.

Over the past decade, the market has moved beyond experimental or niche use cases. Today, VIPs are increasingly found in high-performance buildings, energy-efficient appliances, refrigerated transport, cold storage facilities, and specialized industrial applications. Their ability to reduce energy consumption, optimize internal space, and support sustainability goals makes them particularly attractive in an era of rising energy costs and stricter environmental regulations.

Technological progress has played a crucial role in accelerating adoption. Improvements in core materials, barrier films, and sealing techniques have enhanced durability, thermal stability, and overall reliability. At the same time, manufacturers are investing in more automated production processes to improve consistency and gradually reduce costs, making VIPs more accessible to a wider range of industries.

With governments, businesses, and consumers increasingly focused on energy efficiency and carbon reduction, the vacuum insulation panel market is well positioned to remain a key part of the global insulation and thermal management landscape through 2034.

Vacuum Insulation Panel Industry in Context

The insulation industry is undergoing a structural shift. Traditional materials still dominate in terms of volume, but they are increasingly being challenged by advanced solutions that offer higher performance in thinner profiles. VIPs sit at the forefront of this transition.

In the construction sector, space efficiency is becoming just as important as thermal performance. Urbanization, high land costs, and the push for smarter building design mean that every centimeter counts. VIPs allow architects and engineers to meet strict energy performance targets without sacrificing usable interior space. This makes them particularly attractive for high-rise buildings, renovation projects, and premium residential and commercial developments.

In refrigeration and cold chain logistics, the logic is even clearer. Better insulation means lower energy consumption, more stable temperature control, and more internal storage volume within the same external dimensions. For food, pharmaceuticals, and temperature-sensitive goods, this directly translates into lower operating costs and reduced product loss.

At the same time, sustainability is reshaping material choices across industries. VIP manufacturers are increasingly exploring recyclable cores, low-impact barrier materials, and production methods that align with circular economy principles. This aligns well with global trends toward greener construction, cleaner logistics, and more energy-efficient appliances.

Key Growth Drivers Shaping the Market

Rising Demand for Energy-Efficient Buildings

One of the most powerful forces behind the growth of the vacuum insulation panel market is the global push for energy-efficient buildings. Governments across North America, Europe, and Asia are tightening building codes and introducing stricter energy performance standards to reduce carbon emissions and overall energy consumption.

VIPs offer a compelling solution because they deliver superior insulation performance in a much thinner form factor. This allows developers to meet or exceed regulatory requirements without increasing wall thickness or compromising design flexibility. In both new construction and retrofitting projects, this advantage is becoming increasingly valuable.

Beyond regulations, economics also play a role. Building owners and occupants are more aware than ever of long-term energy costs. High-performance insulation reduces heating and cooling demand, leading to lower utility bills over the life of a building. While VIPs involve higher upfront costs, their long-term savings and performance benefits make them an attractive option for premium and performance-focused projects.

As green building certifications and sustainability benchmarks continue to gain importance, the role of advanced insulation materials like VIPs is expected to expand further.

Expansion of Refrigeration and Cold Chain Applications

The rapid growth of global cold chain logistics is another major driver for the vacuum insulation panel market. From fresh food and frozen products to vaccines and biologics, the world is moving more temperature-sensitive goods than ever before.

VIPs are particularly well suited to this environment. Their excellent thermal performance helps maintain stable internal temperatures while reducing energy consumption. At the same time, their thin profile allows manufacturers to increase usable internal volume in refrigerators, freezers, and transport containers without increasing external size.

The rise of e-commerce grocery delivery, pharmaceutical distribution, and global food trade has only intensified the need for reliable, efficient, and compact insulation solutions. As cold chain infrastructure expands, so does the addressable market for VIPs across transport, storage, and appliance applications.

Technological Advancements and Material Innovation

Continuous innovation is reshaping what vacuum insulation panels can do. Advances in core materials such as silica and fiberglass, along with improvements in barrier films and edge sealing technologies, have significantly improved durability, consistency, and thermal stability.

Manufacturers are also developing more flexible and lightweight panels, making installation easier and opening up new application areas, including appliances, retrofitting projects, and specialized industrial uses. At the same time, automation and process optimization are helping to improve production efficiency and gradually reduce costs.

Sustainability-focused innovation is another important trend. Research into recyclable and lower-impact materials is helping VIPs align more closely with environmental regulations and corporate sustainability goals, further strengthening their long-term market potential.

Challenges Facing the Vacuum Insulation Panel Market

High Manufacturing and Installation Costs

Despite their performance advantages, VIPs remain significantly more expensive than conventional insulation materials. The need for advanced materials, precision manufacturing, and airtight sealing processes drives up production costs. Installation also requires skilled handling to avoid damage that could compromise performance.

For cost-sensitive projects, especially in mass residential construction, this higher upfront investment can be a barrier. While long-term energy savings often justify the cost, the initial price tag still limits broader adoption in some segments of the market.

Durability and Sensitivity Concerns

Vacuum insulation panels are highly efficient, but they are also sensitive to physical damage. A puncture or seal failure can destroy the vacuum and drastically reduce insulation performance. This makes transportation, handling, and installation critical stages in the value chain.

In harsh environments or complex construction projects, ensuring long-term durability requires additional protective measures, quality control, and careful design integration. These factors add complexity and cost, which can slow adoption in certain applications.

Regional Market Perspectives

United States

The United States vacuum insulation panel market is benefiting from strong demand for energy-efficient buildings, advanced appliances, and expanding cold chain infrastructure. Green building initiatives and energy efficiency standards are encouraging the use of high-performance insulation materials in both new construction and renovation projects.

At the same time, growth in refrigerated transport, food logistics, and pharmaceutical distribution is creating new opportunities for VIPs in cold chain applications. Ongoing technological improvements are also making panels more reliable and easier to integrate, supporting steady market expansion across multiple sectors.

Germany

Germany represents one of Europe’s most important markets for vacuum insulation panels, driven by strict energy efficiency regulations and a strong commitment to sustainable construction. Policies aligned with the Energy Performance of Buildings Directive and national energy standards are pushing developers toward higher-performance insulation solutions.

Beyond buildings, Germany’s strong industrial and logistics sectors are also adopting VIPs for refrigeration and cold storage applications. With a mature focus on energy conservation and engineering quality, the German market is expected to remain a key driver of innovation and adoption in Europe.

China

China’s vacuum insulation panel market is growing rapidly, supported by urbanization, large-scale construction activity, and government policies promoting energy efficiency and green buildings. As cities expand and building standards evolve, demand for high-performance insulation materials is rising sharply.

China’s booming cold chain and e-commerce sectors are also fueling adoption in refrigeration, transport, and storage applications. With continued investment in manufacturing capacity and technology, China is likely to remain one of the most dynamic growth markets for VIPs through 2034.

Saudi Arabia

In Saudi Arabia, demand for vacuum insulation panels is being driven by the need for energy-efficient buildings in a hot climate, along with expanding cold storage and logistics infrastructure. High cooling costs and sustainability initiatives are encouraging the adoption of advanced insulation solutions in both residential and commercial projects.

Government programs focused on energy efficiency and sustainable development are further supporting market growth. As construction and logistics investments continue, VIPs are expected to play a growing role in improving thermal performance and reducing energy consumption across the Kingdom.

Recent Developments in the Market

The vacuum insulation panel market has seen several notable strategic moves in recent years. In March 2023, Hutchinson and va-Q-tec announced a collaboration aimed at delivering scalable, high-performance insulation solutions for eMobility applications, highlighting the expanding role of VIPs beyond traditional sectors.

In March 2022, NEVEON’s Specialties business unit expanded VIP production with a new fully automated facility in the Czech Republic, underlining the industry’s focus on scaling capacity and improving manufacturing efficiency. Earlier, in February 2022, Recticel agreed to acquire Trimo, strengthening its position in high-quality insulated panels for the construction sector and expanding its geographic reach.

These developments reflect a broader trend toward consolidation, capacity expansion, and technological investment across the industry.

Market Segmentation Snapshot

The vacuum insulation panel market can be viewed across several dimensions. By type, it includes flat panels and special-shape panels designed for customized applications. By raw material, panels commonly use plastics and metals for barrier structures. Core materials include silica, fiberglass, and other specialized materials optimized for thermal performance.

In terms of application, major segments include construction, cooling and freezing devices, logistics, and other industrial uses. Geographically, the market spans North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, with key growth coming from the United States, Germany, China, and emerging markets in the Middle East and Asia.

Competitive Landscape

The market features a mix of global material science companies, insulation specialists, and technology-driven manufacturers. Key players include Avery Dennison Corporation, BASF SE, Kingspan Group, Etex Group, Panasonic Corporation, Morgan Advanced Materials, Kevothermal, Knauf Insulation, OCI Company, and Evonik Industries.

Competition is increasingly focused on performance improvement, cost optimization, production scale, and sustainability credentials, as companies seek to differentiate themselves in a market that values both technical excellence and long-term efficiency.

Final Thoughts

With the global vacuum insulation panel market projected to grow from US$ 10.65 billion in 2025 to US$ 15.72 billion by 2034, the next decade will be defined by steady adoption across construction, refrigeration, and logistics. While challenges around cost and durability remain, ongoing technological progress and rising demand for energy-efficient solutions are steadily strengthening the case for VIPs.

In a world where energy efficiency, space optimization, and sustainability are no longer optional, vacuum insulation panels are moving from a specialized solution to a strategic material—quietly but decisively reshaping how industries manage heat, space, and energy.

About the Creator

Australia Helicopter Services Market: Steady Growth Fueled by Emergencies, Tourism, and Technological Upgrades

The Australia helicopter services market reached a value of USD 54 million in 2024 and is forecast to grow to USD 68.99 million by 2033, representing a compound annual growth rate (CAGR) of 2.76% between 2025 and 2033, according to the latest IMARC Group analysis.

By Rashi Sharma5 days ago in Trader

It's 2026. Songs Turning 10 This Year

In 2016, we saw the rise of short form videos and what would lead to the birth of TikTok. We cannot forget the Snapchat filters no matter how cringe worthy some of them might have been. It was also the year in which the hit series Stranger Things debuted.

By Jasmine Aguilara day ago in Beat

Comments

There are no comments for this story

Be the first to respond and start the conversation.