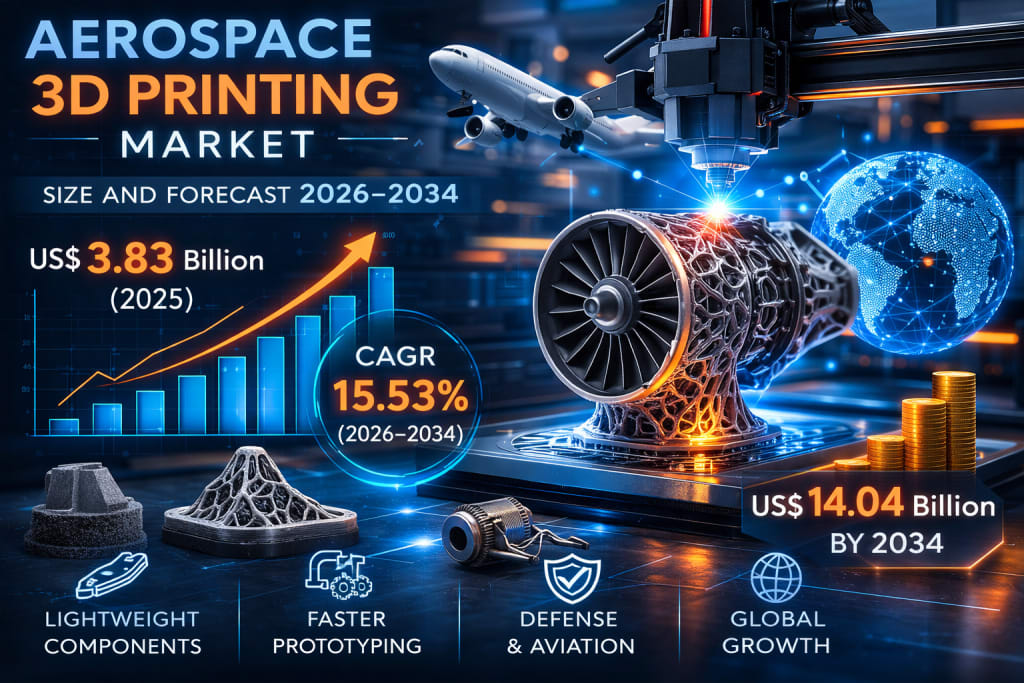

Aerospace 3D Printing Market Size and Forecast 2026–2034

Rising Defense Contracts, Lightweight Aircraft Demand, and Advanced Materials Innovation Propel Additive Manufacturing in Global Aerospace

The global aerospace industry is entering a new era of digital manufacturing transformation, and additive manufacturing is at its core. According to Renub Research, the Aerospace 3D Printing Market is projected to reach US$ 14.04 billion by 2034, rising from US$ 3.83 billion in 2025, expanding at a robust CAGR of 15.53% between 2026 and 2034.

This rapid growth reflects a structural shift in how aircraft and spacecraft components are designed, produced, repaired, and optimized. From defense modernization to commercial aviation efficiency and space exploration advancements, 3D printing is becoming an indispensable pillar of aerospace manufacturing.

Aerospace 3D Printing Industry Overview

Aerospace 3D printing refers to the use of additive manufacturing (AM) technologies to build aircraft and spacecraft components layer by layer using metals, polymers, ceramics, and composite materials. Unlike traditional subtractive manufacturing—which removes material from a solid block—additive manufacturing constructs components precisely where material is needed.

This approach allows for:

Lightweight, topology-optimized geometries

Reduced material waste

Rapid prototyping and iteration

On-demand spare parts production

Supply-chain decentralization

Aerospace companies increasingly use 3D printing to produce engine components, ducts, brackets, structural assemblies, and interior cabin parts. The technology enables consolidation of multiple parts into a single printed component, reducing assembly complexity and minimizing potential failure points.

As global aviation traffic rebounds and defense spending intensifies, additive manufacturing is transitioning from experimental applications to certified, flight-ready production components.

Key Growth Drivers in the Aerospace 3D Printing Market

1. Demand for Lightweight, High-Performance Components

Fuel efficiency remains one of the most critical cost factors in aviation. Airlines and defense operators are constantly seeking lighter aircraft structures to reduce fuel consumption, extend range, and increase payload capacity.

Additive manufacturing enables engineers to design highly complex geometries that would be impossible or extremely costly to achieve using traditional machining. By optimizing internal lattice structures and reducing excess material, manufacturers can significantly reduce component weight while maintaining structural integrity.

Furthermore, part consolidation through 3D printing reduces assembly time, lowers production costs, and enhances reliability. As next-generation aircraft increasingly integrate advanced alloys and composite materials, additive manufacturing is becoming a foundational production tool rather than a supplementary technology.

2. Defense Adoption & Evolving Procurement Models

Defense modernization programs worldwide are accelerating the adoption of additive manufacturing. In November 2024, a landmark competitive contract was awarded for a 3D-printed component designed to protect F-15 aircraft from structural damage—signaling a major shift in procurement strategy within U.S. defense operations.

The U.S. Defense Logistics Agency (DLA) is progressively integrating additive manufacturing into mainstream procurement channels. Historically reliant on exclusive contracts, the move toward competitive sourcing demonstrates growing institutional confidence in AM technologies.

Additionally, in October 2024, the U.S. Air Force awarded Beehive Industries a USD 12.4 million contract to manufacture 3D-printed jet engines for unmanned aircraft. This initiative emphasizes rapid deployment capabilities, cost efficiency, and improved readiness for unmanned defense platforms.

Defense agencies value 3D printing for:

Rapid part replacement

Fleet sustainment

Reduced dependency on global supply chains

Production near deployment zones

As militaries aim to maintain aging fleets while strengthening operational resilience, additive manufacturing is becoming mission-critical.

3. Advancements in Materials & Industrial Partnerships

Material innovation is significantly expanding aerospace 3D printing capabilities. High-performance metal powders, heat-resistant alloys, and ceramic materials now allow production of stronger and lighter components suitable for extreme environments.

In November 2024, Equispheres announced a supply agreement with 3D Systems to integrate advanced aluminum powders with DMP Flex 350 and DMP Factory 350 platforms. Such collaborations improve powder flowability, particle consistency, and overall printing reliability—essential for aerospace-grade certification.

Similarly, in August 2024, NASA’s Marshall Space Flight Center partnered with 3DCERAM Sinto to supply a FLEXMATIC Ceramic Printer C1000. The project focuses on producing advanced ceramic components capable of withstanding space and extreme conditions.

These partnerships reflect a broader ecosystem shift—where material suppliers, printer manufacturers, aerospace OEMs, and research institutions collaborate to accelerate scalable production.

Key Challenges Facing the Market

Certification Complexity & Regulatory Barriers

Aerospace manufacturing operates under stringent regulatory oversight. Every printed component must undergo extensive validation to ensure durability, reliability, and safety. Variations in printing processes, surface finishes, and material microstructures complicate standardization efforts.

Obtaining certification for flight-critical parts significantly increases time-to-market and production costs. Smaller firms often struggle with compliance expenses, slowing widespread adoption.

High Costs & Skilled Workforce Limitations

Industrial aerospace-grade printers require substantial capital investment. In addition to expensive machinery, manufacturers must invest in certified metal powders, controlled environments, and advanced inspection systems.

The industry also faces a shortage of professionals skilled in additive design optimization, material science, and post-processing workflows. Limited access to aerospace-certified materials further constrains scalability.

Despite rising demand, these structural challenges may moderate short-term growth for smaller suppliers.

Regional Market Insights

United States

The United States leads the global aerospace 3D printing landscape, supported by strong defense budgets and advanced manufacturing infrastructure. Major OEMs such as Boeing, Lockheed Martin, GE Aerospace, and Northrop Grumman are deeply integrating additive manufacturing across design, prototyping, and production cycles.

The U.S. Department of Defense heavily invests in additive manufacturing infrastructure to mitigate supply-chain risks and enhance mission readiness. Academic institutions, national laboratories, and private innovators collectively create the world’s most mature aerospace AM ecosystem.

Germany

Germany stands as a major European hub for aerospace additive manufacturing. Companies such as Airbus, MTU Aero Engines, and Siemens actively deploy 3D printing for engine components and structural assemblies.

The country’s strong engineering culture, combined with Industry 4.0 initiatives, fosters continuous innovation in metal AM systems and high-performance alloys.

China

China’s aerospace 3D printing market is expanding rapidly through government-backed aviation programs and defense modernization initiatives. Domestic production of metal powders and large-format printers reduces dependency on foreign suppliers.

The nation increasingly uses additive manufacturing for rocket components, engine parts, and structural assemblies. As aviation demand grows and fleet expansion accelerates, China is positioning itself as a powerful competitor in aerospace additive manufacturing.

Saudi Arabia

Under Vision 2030, Saudi Arabia is actively localizing aerospace and defense manufacturing capabilities. Investments in additive manufacturing centers and industrial training programs are strengthening domestic production capacity.

Airlines and maintenance facilities are exploring 3D printing for spare parts, tooling, and MRO applications to improve operational efficiency and reduce import reliance.

Recent Industry Developments

October 2024: Beehive Industries secured a USD 12.4 million contract from the U.S. Air Force for 3D-printed jet engines for unmanned aircraft.

August 2024: NASA selected 3DCERAM Sinto for advanced ceramic 3D printing collaboration.

April 2024: Relativity Space received USD 8.7 million from the U.S. Air Force Research Laboratory to enhance real-time defect detection in large-format additive manufacturing.

These milestones demonstrate increasing institutional trust in additive manufacturing for mission-critical aerospace applications.

Market Segmentation

By Offerings

Materials

Printers

Software

Services

By Printing Technology

Direct Metal Laser Sintering (DMLS)

Fused Deposition Modeling (FDM)

Continuous Liquid Interface Production (CLIP)

Selective Laser Melting (SLM)

Selective Laser Sintering (SLS)

Others

By Platform

Aircraft

Unmanned Aerial Vehicles (UAVs)

Spacecraft

By Application

Engine Components

Space Components

Structural Components

By End Use

OEM

MRO

Competitive Landscape

Key companies operating in the aerospace 3D printing market include:

3D Systems Inc.

General Electric Company

Markforged

Proto Labs

SLM Solutions Group AG

Stratasys Ltd.

The ExOne Company

VoxelJet AG

Each company competes across five key viewpoints: overview, key persons, recent developments, SWOT analysis, and financial insights.

Final Thoughts

The aerospace 3D printing market is no longer in its experimental phase—it is rapidly becoming a central production technology in global aviation and defense industries. With projected revenues climbing from US$ 3.83 billion in 2025 to US$ 14.04 billion by 2034, the market’s 15.53% CAGR reflects strong institutional commitment and technological maturation.

Lightweight component demand, defense procurement reforms, material innovations, and supply-chain resilience strategies are collectively accelerating adoption. While certification complexity and cost barriers remain challenges, continuous regulatory evolution and ecosystem collaboration are expected to ease scalability constraints over the forecast period.

About the Creator

Keep reading

More stories from shibansh kumar and writers in Trader and other communities.

Server Chassis Market Size & Forecast 2026–2034

The Server Chassis Market is projected to grow from US$ 372.43 billion in 2025 to US$ 488.92 billion in 2034, expanding at a CAGR of 3.07% from 2026 through 2034. The steady rise reflects sustained investments in hyperscale data centers, cloud computing infrastructure, artificial intelligence (AI) workloads, and edge computing networks.

By shibansh kumar3 days ago in Trader

United States Telehealth Market Size, Growth, Demand, Trends and Forecast 2026-2034

United States Telehealth Market Overview The United States telehealth market has emerged as a transformative force in the healthcare industry. Telehealth refers to the use of digital communication technologies such as video consultations, mobile health applications, and remote patient monitoring systems that allow healthcare providers to deliver medical services without requiring in-person visits.

By Jackson Watson5 days ago in Trader

Suzlon Share Price: Insights, Trends, and Investment Perspective

Investors looking for opportunities in the renewable energy sector often keep a close eye on the Suzlon share price. Suzlon Energy Limited is one of India’s leading wind energy companies, with a strong presence in domestic and international markets. Over the years, Suzlon has established itself as a major player in the clean energy space, making its stock a focus for investors interested in both growth potential and exposure to the renewable energy sector.

By Hammad Nawaz6 days ago in Trader

Pearl

1980 something. we all hung out at Pearl and you and i were nothing special, or so i thought. i mean we all danced, drenched in our own sweat, our own saline solution of fear, too many beers, shots, laughter, tears, fucks in the bathroom and i don't know when we began to be afraid. do you?

By ROCK aka Andrea Polla (Simmons)5 days ago in Fiction

Comments

There are no comments for this story

Be the first to respond and start the conversation.